Reinventing Local Banking in the Platform Economy

TL;DR — At a Glance Summary

Community banks don’t need to out-scale the big players to stay relevant. They need to out-connect them.

As the platform economy reshapes financial services, smaller institutions can thrive by focusing on what they already do best: trust, proximity, and real partnership with small businesses.

This article explores how banks can:

- Adopt a platform mindset to connect clients with value beyond lending.

- Build strategic partnerships with fintechs and trusted providers to reduce friction and extend reach.

- Use data responsibly to personalize service while strengthening trust.

- Deliver sticky, everyday banking experiences that keep small businesses coming back.

Reinvention isn’t about complexity; it’s about simplicity that scales.

[Image 02: Layer soft graphic elements — light tech overlays, simple line icons — to show the digital dimension subtly with the text overlay "The platform paradox"]

Everywhere we look, platforms dominate. From San Francisco to Singapore, technology companies have redefined how businesses operate and how customers engage.

In retail, Amazon connects buyers and sellers; in payments, platform businesses like Stripe and Square bridge small firms and financial services.

Banking is now entering the same phase of transformation. As digital platforms shape the expectations of small businesses, the challenge for community banks isn’t simply digital transformation; it’s staying essential in a world where value is shared, not owned.

Large financial institutions and fintech giants have the scale, but community bankers still hold something harder to replicate: trust, local knowledge, and personal relationships.

Reinvention starts when smaller players learn to compete not by copying larger institutions, but by connecting better than they do.

What the Platform Economy Means for Banking

A platform economy is built on access and interaction. It rewards the institutions that can leverage technology to connect customers, third-party service providers, and data into shared systems of value.

For banks, this means moving from isolated financial products to integrated services that live within broader networks of economic and social activity.

Across the global economy, we see it happening already: peer-to-peer lending, digital payment services, and open banking APIs have blurred the line between traditional banks and other financial service providers.

Regulators such as the Federal Reserve Bank, the European Commission, and the federal government are now encouraging collaboration through frameworks that promote financial inclusion and economic growth.

For smaller banks, this new landscape brings both opportunity and risk. Technology costs, compliance requirements, and cyber threats are rising, yet so are the possibilities to reach new markets, boost productivity growth, and strengthen local economies.

Why Local Still Matters

In an increasingly digital global economy, proximity still counts.

Community banks and other institutions remain vital because they understand the realities of small business banking in a way larger institutions don't. The seasonality, the family ties, and the role of credit in sustaining economic and social activity at the community level are just a few of the many reasons people still prefer local banking.

According to the Federal Reserve Bank, community lenders provide a significant number of small loans that fund main-street businesses and stabilize bank deposits across rural and urban regions alike.

These relationships don’t just finance growth; they create trust and resilience during uncertainty.

Technology should amplify that advantage, not erase it.

In this digital era, the most successful financial institutions will be those that merge digital technology with human connection, making data work for relationships rather than the other way around.

From Product Providers to Platform Partners

To stay competitive, banks must think less like product manufacturers and more like platform owners.

That means designing business models that enable collaboration with third-party providers, fintechs, and other banks to create seamless ecosystems of value.

Instead of trying to build everything internally, banks can form third-party partnerships to deliver complementary products and services, such as payroll, accounting, HR, or insurance, within their existing digital experience.

This approach reduces operational costs, accelerates innovation, and improves customer stickiness through everyday relevance.

Platforms like Proven were built precisely for this shift. The tool allows banks to curate trusted vendors and third-party relationships under their own brand, turning digital tools and new technologies into tangible client benefits without the overhead of custom development.

By simplifying due diligence and vendor management, community banks can focus on what matters most: serving clients better and helping small businesses grow sustainably.

Rethinking Growth Metrics

In this new environment, traditional KPIs such as loan volume, deposits, and branch expansion no longer capture the full picture.

Modern financial services are measured by value capture, engagement, and shared outcomes.

Platform businesses don’t count success by what they sell, but by how effectively they attract users and keep them active. For banks, this means tracking metrics like ecosystem participation, cross-service adoption, and the lifetime value of connected relationships.

Here, data analytics and artificial intelligence provide a competitive edge. By turning financial data into actionable insight, banks can anticipate client needs, improve credit risk decisions, and personalize advice that drives loyalty.

The result is lower attrition, deeper trust, and greater sustainable growth across the overall economy.

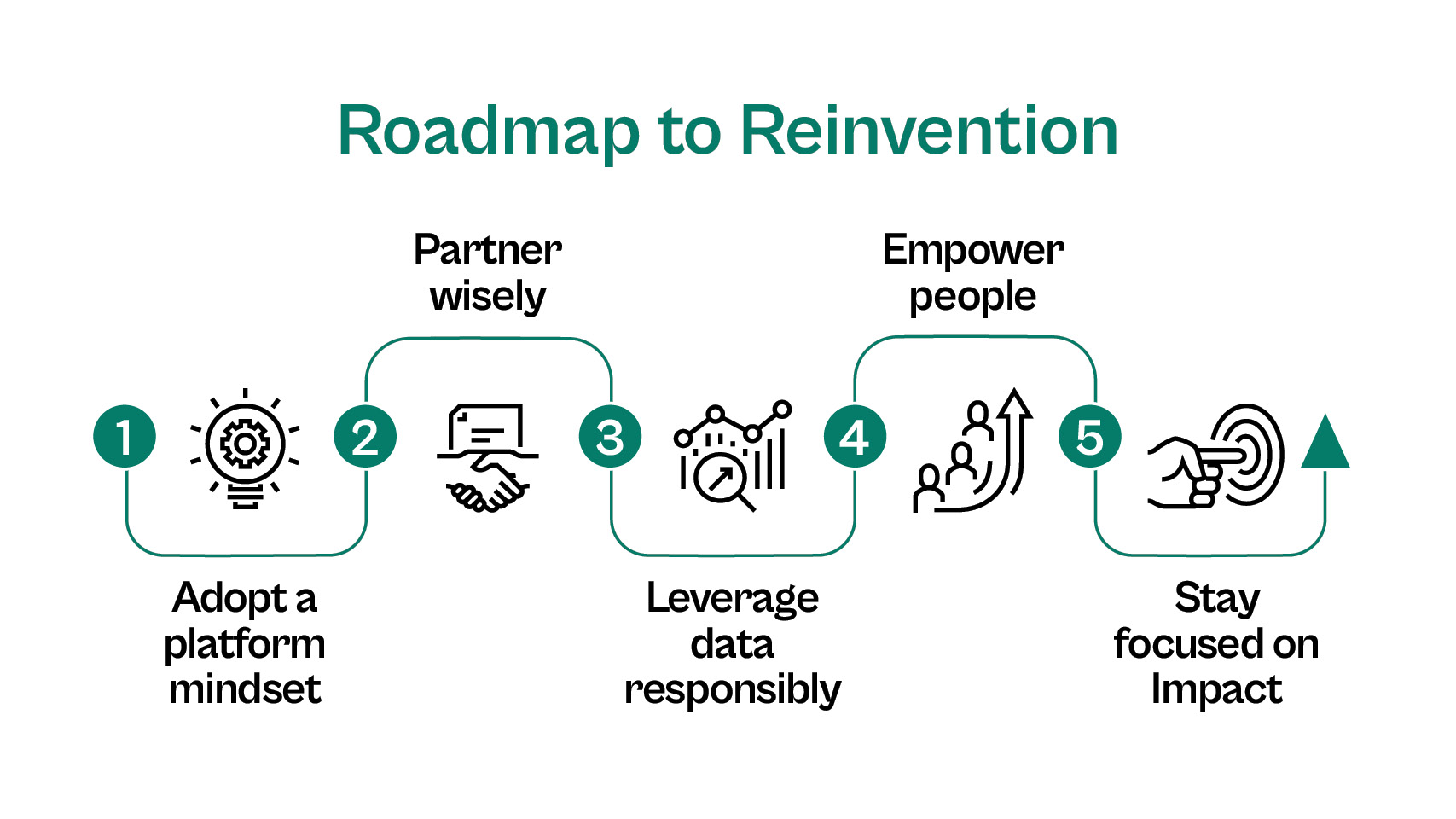

Roadmap to Reinvention

Reinvention doesn’t require a massive overhaul of infrastructure or a billion-dollar innovation fund.

For community banks and smaller financial institutions, transformation happens through a clear strategy, steady action, and a willingness to think differently about where value comes from.

Below is a practical roadmap for how banks can evolve their role from product providers to connection enablers without losing the trust and local relevance that define them.

1. Adopt a Platform Mindset

Reinvention begins with mindset.

Traditional banking structures were built on control through ownership of every system, every product, and every relationship. But the platform economy rewards openness and connectivity.

Adopting a platform mindset means asking, “How can we create value through others, not just through ourselves?”

That could mean sharing APIs with third-party providers, partnering with fintechs, or curating resources that help small businesses operate more efficiently.

It’s not about competing with tech companies; it’s about using collaboration as a strategic advantage to serve your clientele better.

2. Partner Wisely

Every partnership is a reflection of your brand. The goal isn’t to work with as many providers as possible, but with the right ones. Choose those that complement your mission and strengthen your business models.

Forming thoughtful alliances with fintechs, third-party service providers, and other banks allows smaller institutions to deliver more holistic products and services without bearing the full technology costs.

Before onboarding partners, apply rigorous due diligence to assess reliability, security, and cultural alignment. Beyond ensuring the partner is a strong fit for your brand, also consider how well they resonate with your existing clientele. You want them to think "it's about time you partnered with this firm," not "why in the world have you associated with them?"

Strong partnerships don’t dilute or jeopardize identity; they reinforce it by extending trust through credible collaboration.

3. Leverage Data Responsibly

In a connected banking ecosystem, data is the bridge between digital efficiency and personal connection.

Using data processing, data analytics, and even artificial intelligence responsibly enables banks to understand customer patterns, predict needs, and personalize outreach.

But more isn’t always better. The key here is relevance. You want to turn information into insight that makes the customer experience simpler and more enjoyable.

Regulators are increasingly attentive to how banks manage privacy, so clarity and consent must anchor every decision. When handled with transparency, data becomes a compliance asset and a trust asset.

4. Empower People

Transformation fails when technology outruns culture.

Reinvention succeeds when employees are empowered to use digital tools confidently and creatively. That means training your relationship managers and branch teams to see these tools not as replacements for service, but as extensions of it.

Practical steps include integrating AI-driven insights into customer conversations, automating low-value tasks, and ensuring front-line teams have access to real-time customer context.

When people feel capable and connected, innovation spreads naturally from within.

5. Stay Focused on Impact

Ultimately, reinvention is about outcomes, not optics. The best measure of progress is less about the number of new platforms launched and more about how effectively you improve SME access to essential services, funding, and advice.

Monitor how these changes impact client satisfaction, loan turnaround times, and local economies.

A bank that grows alongside its community, rather than outside it, builds resilience that no larger institution can replicate.

In this model, agility becomes the new scale. Smaller banks that act decisively can outperform slower, more complex competitors and prove that relevance, not size, is the true marker of leadership in the digital era.

Small Business Banking That Sticks

For all the technology and transformation taking place, community banking has always been about something simple: relationships that last.

When banks talk about “sticky” customers, it’s easy to focus on products and adding a new account, app, or feature. But true loyalty doesn’t come from features; it comes from familiarity. It comes from being part of a customer’s daily rhythm, not just their quarterly review.

Think about how Amazon became part of everyday life. It didn’t do it by selling more than everyone else. At first, it did so by removing friction from the way people shop.

Every click, every recommendation, every delivery made life a little easier. Over time, the brand became a habit, not a choice.

That’s the mindset community banks can adopt.

In a community bank, loyalty is built the same way: by finding the small moments where clients spend effort, time, or energy and making them smoother. Whether that means integrating bookkeeping tools, streamlining payroll, or connecting them to local service providers, it’s all about relevance.

The goal isn’t to grow big alone, but to find leverage that keeps your bank woven into the daily lives of your customers.

When clients see their bank helping them beyond withdrawals, deposits, and loans, they stop thinking of it as a service provider and start seeing it as a partner in running their lives and business.

That’s how a bank becomes sticky, not through aggressive cross-selling, but by earning its place in the customer’s everyday world.

The question, then, isn’t whether community banks can create this kind of everyday connection, but rather how they can do so consistently without adding more complexity to already-stretched teams and systems.

That’s where the right kind of platform makes all the difference.

The Proven Perspective in Making Partnership Practical

Proven was designed for exactly this kind of work: helping banks become a part of their clients’ daily business life without overhauling their technology or retraining their teams.

It gives banks a simple way to curate and connect trusted vendors, advisors, and tools under their own brand, turning the platform model into something practical, local, and human.

Instead of trying to be everywhere at once, banks can use Proven to be present where it matters most: in the everyday tools, workflows, and decisions that shape their clients’ success.

It’s not about replacing personal relationships. Instead, it’s about giving them more reach and relevance in a digital world.

Conclusion

The most successful banks in this new era won’t be defined by how much they own, but by how well they connect.

When community banks use technology to deepen relationships rather than replace them, they don’t just keep pace with change; they help shape it.

That’s the heart of modern community banking: staying close, staying useful, and staying trusted in a world that’s moving fast.

Relevance today isn’t about being the biggest. It’s about being there as part of your clients’ everyday story, steadily helping them grow.

See how Proven helps banks turn that kind of connection into everyday value by making partnership simple, personal, and scalable.

Browse more topics from this article

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

.png)