How Banks Can Empower Small Businesses Beyond Traditional Services

At a Glance

In today’s crowded financial landscape, community banks have a rare opportunity to redefine their role from pure lenders to trusted connectors.

By building value-adding ecosystems, banks can help small businesses simplify daily operations, strengthen relationships, and access trusted vendors through secure digital platforms.

The future of SME banking won’t be built on more products or complexity, but on clarity, connection, and purpose, where technology enables trust, and simplicity drives growth.

For decades, banks defined success by the number of products and services they sold. These included savings accounts, loans, cards, and the rest of the familiar catalogue.

But as the financial services industry shifts, that model feels incomplete.

Today’s businesses, from a local café to an e-commerce store, expect their bank to help them manage more than money; they want guidance, access, and connection.

Across the banking sector, leaders are asking the same question: how do we stay relevant to clients whose financial lives are spread across multiple vendors and digital tools?

The answer lies in building value-adding ecosystems. These are networks that connect clients to trusted vendors, insights, and resources that help them run and grow their business every day.

Why Do Banks Need to Start Thinking Like Ecosystem Builders?

Running a small business today means juggling a dozen moving parts at once. Costs are rising, interest rates keep shifting, and compliance never stands still.

Most owners are bouncing between online stores, invoicing tools, payroll platforms, and ad dashboards — logging in, logging out, paying fees, repeating the cycle every day.

And in that daily chaos, banks have a rare chance to make a difference: by simplifying how it all connects.

Financial institutions already have what those other platforms lack, namely, customer trust, regulatory strength, and an established business model built on security and relationship-driven service.

By partnering (through strategic partnerships) with technology providers and local experts, banks can turn that trust into a win-win where clients gain simplicity, and the bank deepens customer relationships.

Industry research reveals that nearly eight in ten SMEs say access to integrated digital services influences their choice of bank. That’s not a passing trend, it’s an effective strategy for survival in a competitive market.

The Power of Local Ecosystems

Community banks and credit unions are uniquely positioned to lead this shift toward value-adding ecosystems. They already understand their regions, their clients’ core operations, and the rhythm of local commerce in a way that larger institutions and fintechs can’t easily replicate.

But the real advantage lies in trust. Local business owners still see their bank as a cornerstone of their financial lives, a familiar face that has weathered the same economic uncertainty they have. That trust gives community institutions a foundation to extend value beyond traditional banking.

By connecting their clients with verified accountants, HR firms, marketing agencies, or technology vendors through a secure online platform, banks move from being service providers to connectors of growth. This approach transforms how small businesses operate, saving them time, reducing costs, and providing vetted expertise they can rely on.

Imagine a small design studio that’s outgrown its own store and needs to expand its online presence. The owner knows how to design logos but not how to manage taxes, process payments, or handle international transactions.

A nearby community bank steps in—not with another loan offer, but by giving the owner access to a curated digital marketplace. Through the bank’s secure hub, the business can connect with a local accountant, find an affordable e-commerce platform, and set up payroll support, all in one place.

For the studio, that’s more than convenience; it’s confidence. For the bank, it’s a stronger customer relationship built on tangible support.

This is how community banking evolves: by blending local understanding with digital simplicity.

The ripple effect is significant. When community banks help their clients grow, they also strengthen the local economy. Money stays within the region, new jobs emerge, and customer trust deepens with every interaction. That’s the real promise of a value-adding ecosystem. It is a model that turns community insight into shared growth.

In this way, community institutions can compete not by mimicking global fintechs, but by offering something those firms can’t: a human network that’s powered by technology, rooted in place, and built on relationships.

From Transactions to Relationships

For an industry obsessed with products and transactions, it’s easy to forget what keeps customers loyal: relationships built on value.

Technology can automate processes, but it can’t replace the confidence a small business owner feels when their bank understands their world. The next wave of success in community banking will come from rethinking the bank’s role not as a place where payments are processed, but as a partner that helps clients manage and grow their businesses.

That shift starts with focusing less on what you sell and more on what you enable.

Banks that offer access to a curated marketplace of trusted vendors (for everything from payroll and marketing to accounting and data analytics)extend their core offerings without reinventing their infrastructure. Every interaction becomes more meaningful: when a client logs in, they see opportunities, not just balances.

Illustration:

Consider a small retailer that runs both a physical location and an online store. Their main challenge isn’t just handling daily transactions, it’s managing inventory, marketing, and customer communication across channels.

If their community bank offered them a digital marketplace, where they could easily access an affordable inventory platform, connect to a vetted shipping provider, and even find tools for running targeted Google Ads campaigns, what are the chances the client would want to migrate to a newer bank just because they were offered lower interest rates?

For the retailer, that experience provided by their current bank is invaluable and feels seamless: one bank, many solutions, less stress.

For the community bank, it’s a deeper relationship that extends far beyond lending. It's a model where technology creates space for human connection instead of replacing it. This is the essence of value-adding ecosystems.

They transform the customer experience from a once-a-month statement review into an ongoing partnership for growth. And when that happens, loyalty becomes organic, not because of lower fees or interest rates, but because the bank genuinely makes life easier.

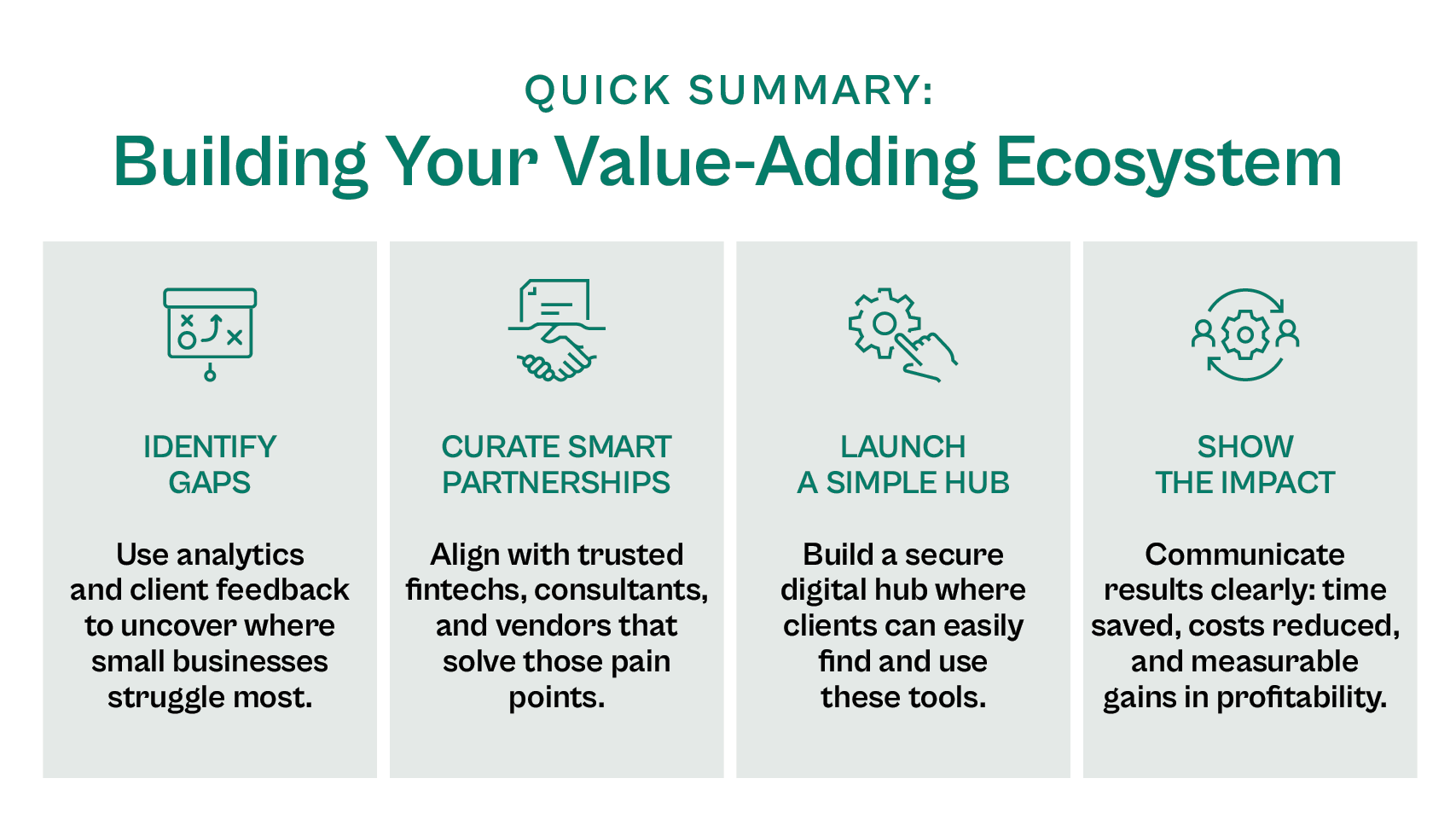

Practical Blueprint for Building Your Value-Adding Ecosystem

Building an ecosystem doesn’t require reinventing your business model. It starts with using what your bank already does best: understanding clients, connecting partners, and earning trust.

Here’s how to turn those strengths into a structured, scalable approach.

1. Map Your Clients’ Gaps

Start by identifying where your business clients struggle most. Use data analytics and frontline feedback to pinpoint recurring friction points, whether it’s cash-flow visibility, compliance challenges, or a lack of reliable marketing support.

Often, the gaps aren’t about access to capital but about access to capabilities.

For example, a manufacturer may not need another loan, but they would be eager to receive trustworthy solutions that make it easier to manage invoices and payments from multiple vendors. Understanding those operational pain points will guide which partnerships and tools matter most for your banking platform.

2. Curate the Right Partners

Once you know the needs, look outward. Forge genuine partnerships with fintech providers, local consultants, and vetted marketplace vendors who can fill those gaps.

This is your digital neighborhood, a network of trusted experts who complement your own products and strengthen the bank’s overall offer.

Strong strategic partnerships should share your standards for security, service, and customer trust. And they don’t have to be complex: even a few high-quality collaborations can deliver more tangible value than a dozen scattered tools.

3. Launch a Simple Hub

Bring it all together through a single, secure online platform. We call this your digital vendor marketplace. Here, clients can easily access accounting, payroll, or marketing resources in one place, with clear descriptions and transparent pricing. In many cases, you might even unlock special discounts and perks that they would otherwise not receive as individual buyers.

The goal isn’t to sell more, it’s to help clients manage their core operations without jumping between systems. That simplicity enhances customer experience, saves time, and strengthens the bank’s position as the central partner in each client’s business journey.

4. Communicate the Value

A great ecosystem only works if people know about it. Promote the hub as part of your broader customer experience strategy, not as an add-on.

Show how the ecosystem saves time, reduces costs, and improves profitability for local businesses and why your bank is uniquely qualified to bring it all together. Highlight early success stories. For instance, if a client increased their revenue by integrating a new payment or HR tool through your marketplace, tell that story. It proves that your ecosystem isn’t just digital infrastructure, it’s a growth engine for your community.

Turning Vision Into Execution

For many financial institutions, the hardest part of ecosystem building isn’t seeing the opportunity; it’s bringing it to life.

Most leaders already recognize that small businesses need better access to trusted vendors, digital tools, and expertise. The problem is that connecting all of those pieces can quickly become a complex project that demands new systems, integrations, and coordination across departments.

That’s why simplicity matters as much in execution as in strategy. The best approach is one that builds on what the bank already does well: its relationships, its understanding of the community, and its ability to deliver value safely.

Some banks are addressing this by creating small, secure digital hubs where business clients can find verified partners, curated resources, and practical tools for managing their operations, all in one place. Others are exploring ready-made platforms that make this kind of implementation faster and less resource-intensive.

What matters most isn’t the technology itself, but the intent behind it: helping customers solve real problems without adding new complexity. That’s the heart of value-adding ecosystems, and it’s where banks can move from concept to impact quickly.

Before we look ahead to how technology is reshaping the banking industry, it’s worth remembering that innovation doesn’t have to be complicated. That’s the principle behind Proven, a platform we built specifically to make simplicity scalable.

Instead of adding layers of technology, it gives banks a straightforward way to connect clients with trusted vendors, tools, and services inside one secure hub. It’s designed to complement, not replace, the human relationships that community institutions are built on.

Explore Proven's marketplace to learn what's possible for your bank.

What Really Drives the Future?

In the financial services industry, technology and trust will drive the future. And it will be shaped by advances in digital banking, data analytics, and emerging forms of automation and generative AI.

But even as technology grows more powerful, it’s easy for banks to lose sight of what actually builds loyalty: trust, clarity, and the human connection.

Now more than ever, the best financial institutions use technology to simplify, not complicate, their clients’ experience. They deploy tools that make life easier, transactions more secure, and decisions more informed. They focus on helping business owners see their finances in context, not just as numbers on a screen.

When used this way, technology becomes a bridge rather than a barrier. AI and automation can anticipate needs, streamline communication, and even flag opportunities, but they should always serve people, not replace them.

The same principle applies to data. The goal isn’t to overwhelm customers with dashboards and metrics but to deliver clarity they can act on. When banks use analytics to tell a simple, transparent story about their clients’ financial lives, they reinforce trust and position themselves as indispensable partners.

Ultimately, the banks that thrive won’t be those with the flashiest technology, but those that make innovation feel intuitive, safe, and personal.

Technology as an enabler and trust as the foundational layer. That's the real differentiator.

Looking Ahead: How Banks Can Help Businesses Thrive

As the financial services landscape evolves, banks are being asked to support clients in ways that go far beyond credit and cash management.

Across industries (from the ecommerce store owner shipping products abroad to international businesses navigating cross-border payments), small firms are operating in more complex markets with thinner profit margins and higher expectations from consumers.

The next five years will bring even more emerging trends that reshape how business banking works.

Advances in artificial intelligence will make forecasting, management, and personalized advice more precise. Digital products and platforms will redefine how entrepreneurs build revenue streams and meet customers online. And as the line between local and global business continues to blur, banks that understand these unique challenges will be the ones best positioned to guide growth.

This creates both pressure and opportunity for institutions: the pressure to keep pace with change, and the opportunity to lead it by offering clarity and practical support.

Helping clients improve revenue growth isn’t just about lending,;it’s about meeting customer needs through insight, partnership, and modern tools that make success sustainable.

Conclusion

The most powerful change happening in banking right now is relational. The institutions that will thrive aren’t the ones with the most code in their systems, but the most connection in their communities.

As small businesses navigate tighter margins, faster markets, and constant uncertainty, they’re looking for a partner who helps them cut through the noise, someone who can turn fragmented tools into a single, trusted experience.

That’s the real opportunity for today’s banks: to become builders of ecosystems, not just brokers of capital. To use technology as a bridge. To bring simplicity to a world that keeps adding layers.

Because the future of banking isn’t about who innovates first, it’s about who makes innovation feel effortless. And the institutions that master that balance will become more than banks.

They’ll become the invisible infrastructure behind small business success.

What if your bank became the platform that helps local businesses bank better and grow faster?

Browse more topics from this article

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

.png)